The Blum Firm’s Approach to Saving Taxes

I often describe The Blum Firm as taking a “head & heart” approach to tax and estate planning. Most of my weekly blog posts veer more to the heart side, focusing on how to create and pass down a meaningful family legacy. Today’s post shifts more to the head side, describing The Blum Firm’s approach to helping our clients save tax. For the first 35 years of my career, saving tax was almost my only focus. Over the last decade, we’ve expanded our focus to help families create a thoughtful inheritance and pass it down to heirs who are prepared to receive it—not just preparing the money for the family, but also preparing the family for the money. The two work hand-in-hand.

Tax planning is still an important part of that equation. Let me give you a couple of real-life examples that illustrate our approach to helping clients save tax.

- The new director of a family office insisted that the family get a second opinion on their estate plan. The family resisted, as they had been working with a reputable law firm for decades and were convinced they were “all set.” The family office director persisted, and they hired The Blum Firm to review the plan. To the family’s amazement, we discovered numerous missed planning opportunities. The family hired us to implement a series of transfers to trusts, including a sale to a grantor trust in exchange for a note, a sale to a grantor trust in exchange for a private annuity, and a charitable lead trust. When the matriarch died about two years later, the IRS audited the estate and upheld the planning we did. The director of the family office did the math: our planning saved the family approximately $1 billion in estate tax.

- An elderly matriarch was in hospice care and seeking last-chance planning to help save estate tax. We informed the family of options, including a private annuity technique that would only be available if she had a greater than 50% chance of surviving a year. Although not a tool that was initially available to her, she remarkably rallied (even booked a vacation) and we instantly implemented it. Several months later, she fell and soon thereafter died. The IRS initially challenged the plan because she didn’t live a full year after doing it. We defended the estate by asserting that the test was not whether she actually lived a year, but whether at the time of the transaction, she had a likelihood of living a year. The IRS later offered to settle the case by accepting 20% of the amount of the tax, saving the family 80% of the tax they would’ve owed had they not planned. The family saved millions of dollars and never had to go to court or talk to the IRS.

These are just two examples of many such cases, but they give a flavor of our approach to planning. We only propose techniques that are supported solidly under the law. We disclose everything to the IRS on gift tax returns, activating a statute of limitations that gives the IRS a three-to-six-year time frame to assert gift tax. In all my 46 years of practicing law this way, other than the one 20% concession described above (which was a big win for the family), The Blum Firm has never had to make a concession to the IRS, other than valuation adjustments. That track record is very important to us.

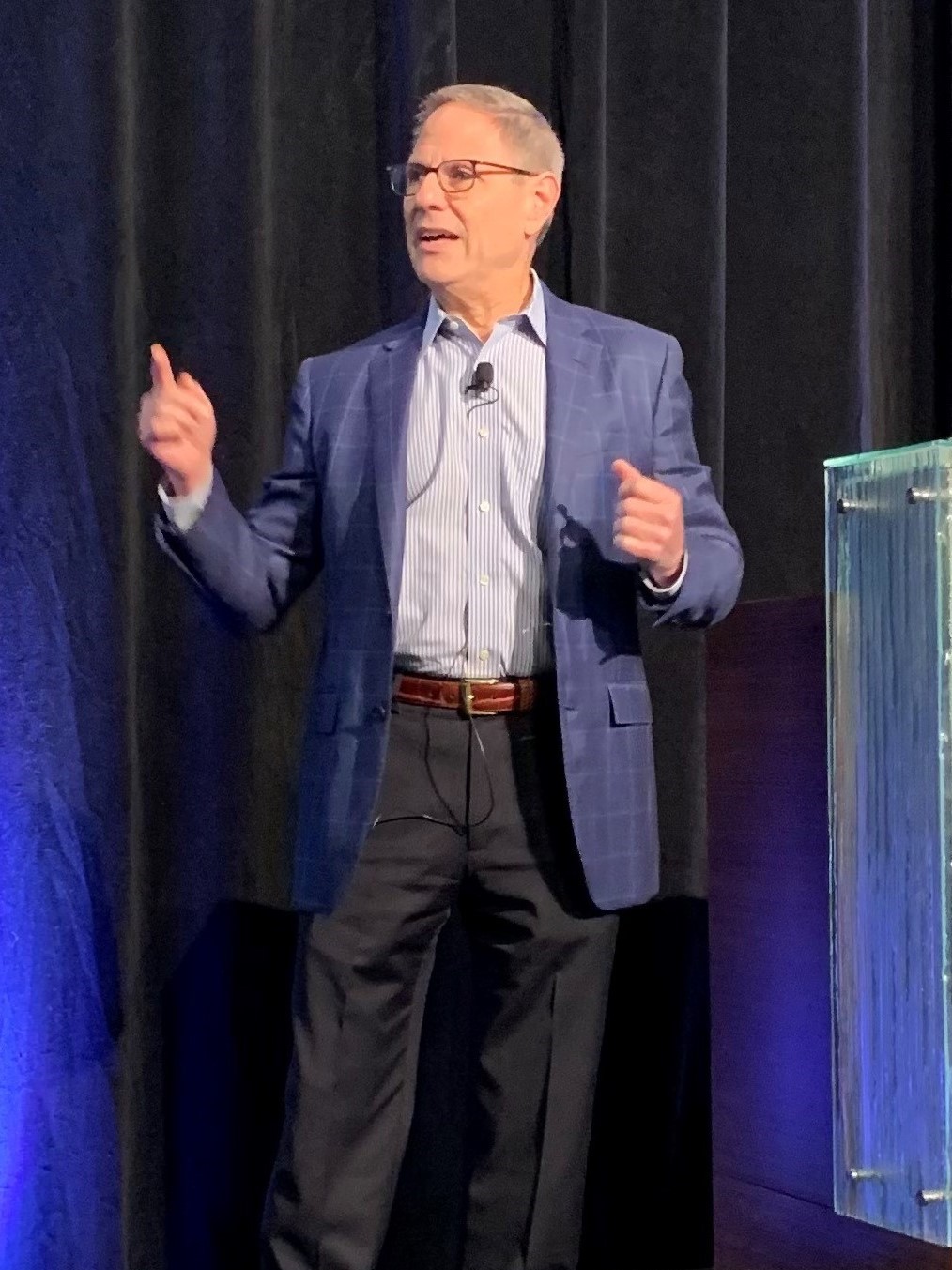

In addition to work to save estate taxes, we are equally committed to helping clients save income taxes. Saving income tax is harder because there are fewer tools in our toolbox, but we have devised multiple strategies to save income tax. I recently spoke to the Midland-Odessa Business & Estate Council on “Creative Income Tax Strategies.” Click this LINK to see the PowerPoint from that speech.

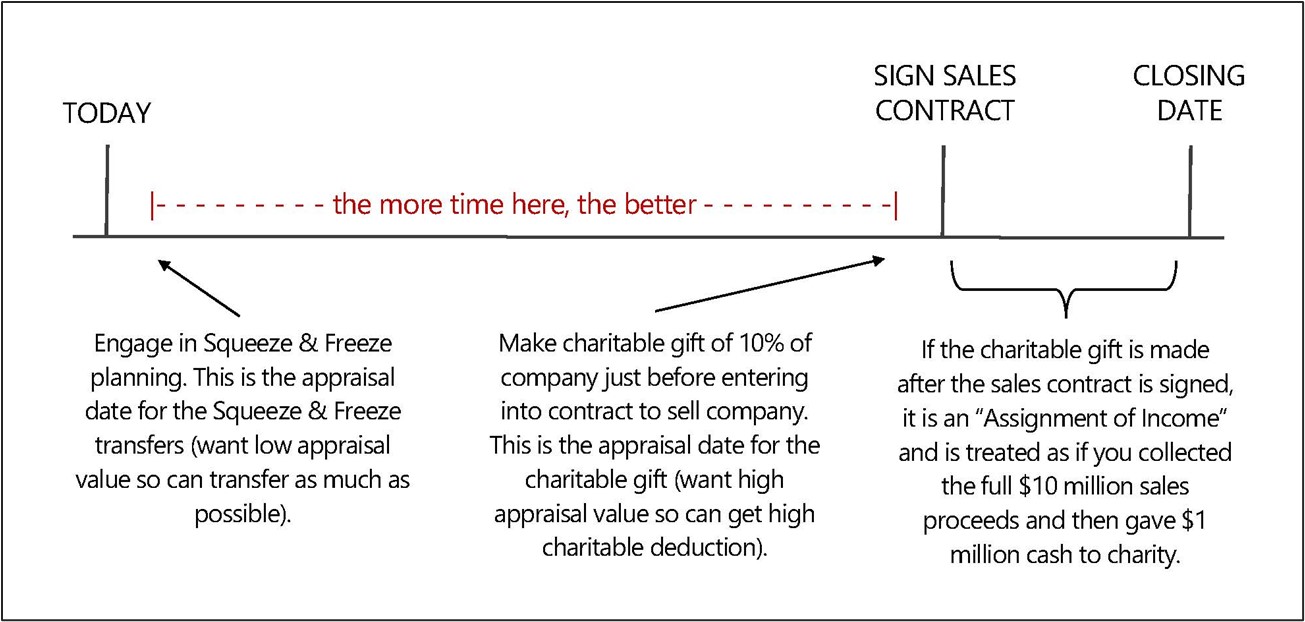

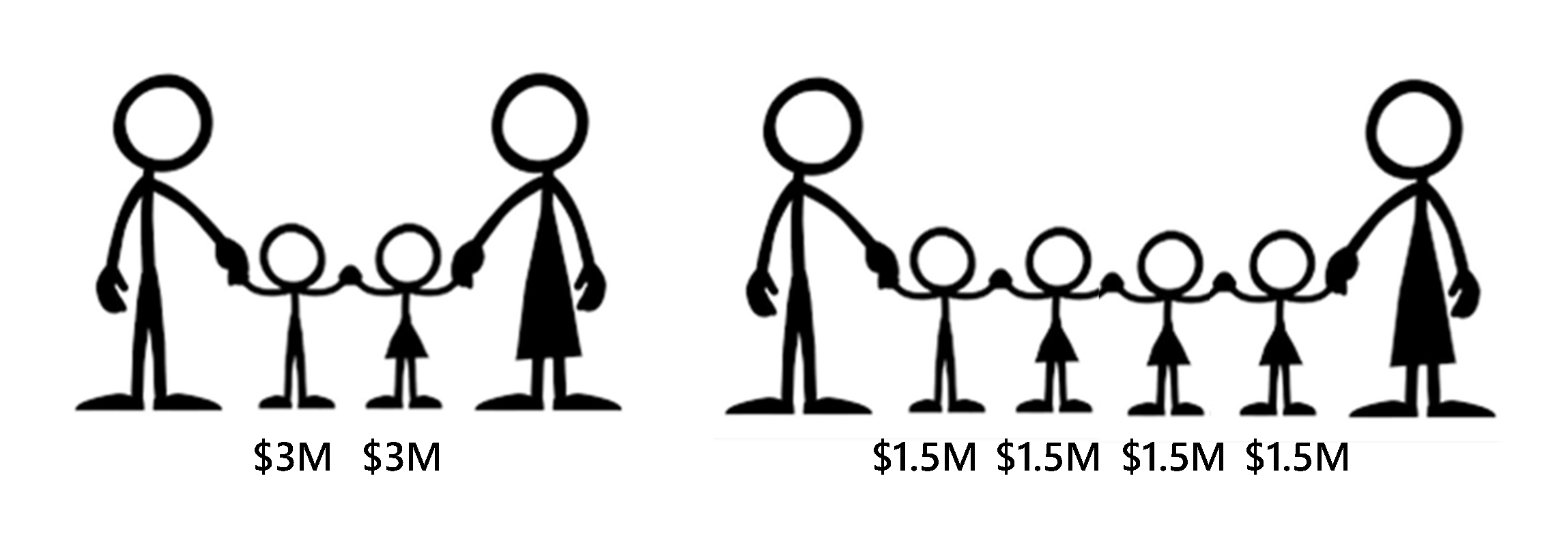

Some of the tools in my speech take advantage of opportunities in the law to avoid income tax, such as Roth IRAs, Qualified Small Business Stock (“QSBS”), and Private Placement Life Insurance. Other tools, such as Mixing Bowl Partnerships and Upstream Basis Planning achieve a free basis step-up on assets (and unlike the normal basis step-up, you don’t have to die to achieve it). Others achieve a tax deferral, such as Charitable Remainder Trusts and Installment Sales (where I illustrated a way to achieve a 23-year tax deferral). We have designed ways for people (who might think they aren’t a fit) to qualify for these tools and save substantial amounts of income tax. For example, if you expect to sell a business five or more years from now and your ownership interest isn’t currently structured as QSBS, there are multiple ways to convert into QSBS and avoid tax on $10 million (or far more) of the gain. And if you do own QSBS and are about to sell your business, consider gifting stock to non-grantor trusts so that in addition to avoiding tax on $10 million of gain on the stock you own, each trust can also avoid tax on $10 million of gain.

This type of planning isn’t as simple as going through a simple checklist of tools. It requires a case-by-case analysis, reviewing your assets and entity structure to explore the many possibilities. One more word to the wise: we can do more to help when the call we receive is in future tense, discussing an asset you are planning to sell or planning to acquire, rather than a past tense call about something you already did. It’s never too late, but the earlier in the timeline you start, the more opportunity we have to help.

Marvin Blum was honored to speak on "Creative Income Tax Strategies" at the Midland-Odessa Business & Estate Council.

{kind=link}