In my series on Business Succession Planning, I’ve identified three choices for transfer of a business: (1) transfer to family members; (2) sale to employees/insiders; and (3) sale to an outside third party. After a candid assessment, it often becomes clear that the first choice isn’t a workable option. That leaves the owner with a sale of the business, whether to inside parties or outside parties.

When an owner sells a business, it frequently is the first time the family has substantial liquid assets. That’s why the sale of a business is commonly referred to as a “Liquidity Event.”

On a light-hearted note, I’ve kidded with my wife Laurie that so many of the men I represent who’ve had a liquidity event go buy a bright blue blazer and seem to wear it everywhere they go. Laurie and I call it a “Liquidity Blazer,” and I lamented that I’ll never have a liquidity event enabling me to buy one. We were having this conversation when I was in Las Vegas to give a speech, walking around Caesar’s Mall to pass the time (since you won’t find me at a gambling table). There in the window of Brooks Brothers was the Liquidity Blazer of my dreams, and Laurie made me try it on—perfect fit, no need for alterations. Laurie convinced me that (even without a liquidity event) I deserved it, and I wore it the next day when I gave my speech.

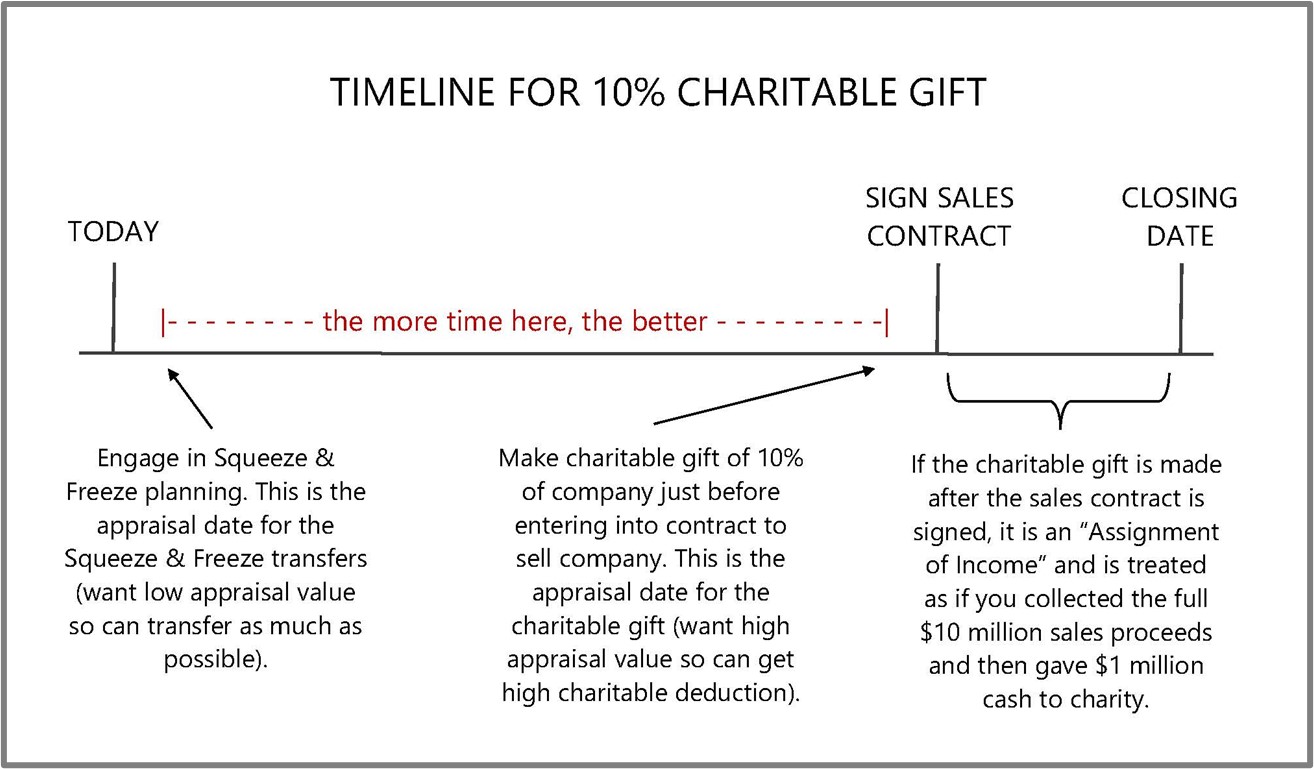

On a more serious note, selling a business also provides the owner with the liquidity to satisfy long-held desires to make substantial charitable contributions. All too often, business sellers contact me AFTER the sale has closed for charitable giving guidance. If only I could wind the clock back, there’s a better order of events that could’ve saved them a lot of tax. Consider this example: Owner sells business for $10 million and then donates $1 million to charity, leaving the owner with $9 million before tax. Owner reports income of $10 million (for simplicity, assume a zero basis), and takes a deduction for the $1 million charitable gift, paying tax on $9 million. Rewind the clock: owner donates 10% of the business just prior to entering into the sales contract. At closing, owner receives $9 million, and the charity receives $1 million. Owner reports income of $9 million and takes a deduction for the charitable gift of a 10% slice of the business (appraised at close to $1 million in value), paying tax on approximately $8 million. Bottom line: by making the gift to charity BEFORE the sale, owner saves income tax on $1 million of the sales proceeds.

The following chart illustrates this timeline. To supercharge the family’s tax savings, note the recommendation to do “squeeze & freeze” planning well in advance of the sale. Such planning shifts the business into trusts that are out of the estate, avoiding the 40% estate tax at death. There are trust structures that allow you to achieve this outcome, yet retain access, control, and flexibility. The most popular trust options are SLATs, 678 Trusts, DGTs, and GRATs. Also note that making the charitable gift too close to the closing date runs the risk of an “assignment of income,” killing the above-described tax benefit. Also, be aware that a pre-transaction charitable gift of a family business needs to be made to a public charity or donor advised fund, in order to deduct the fair market value of the gifted business interest. Consult a tax advisor to help you achieve the best tax outcome.

To take these tax savings up to the limit, consider these two recent examples where the owner gave away the ENTIRE business: electronics giant Tripp Lite ($1.6 billion value) and outdoor apparel maker Patagonia ($3 billion value).

- Barre Seid donated 100% of Tripp Lite to Marble Freedom Trust, a non-profit devoted to conservative causes. After the donation, the company was sold for $1.65 billion, with all the proceeds going to Marble Freedom Trust free of income tax.

- The Chouinard family donated 2% of their Patagonia stock (all the voting shares) to a new Patagonia Purpose Trust, and 98% of their stock (all non-voting) to Holdfast Collective, a non-profit devoted to protecting the environment.

Neither family will pay any tax when Marble Freedom or Holdfast sells the business it owns, and all the proceeds will be committed to causes important to that family. Ironically, those causes are opposite: Marble Freedom funds efforts to stop action on climate change; Holdfast funds efforts to combat climate change. That’s yet another example of the polarized world we’re living in today. [Note that since these two nonprofits are politically focused, they are 501(c)4 rather than 501(c)3 organizations, so the contributions to them are not deductible, but the income they earn is exempt from tax. Furthermore, supporters can donate assets that the 501(c)4 sells and avoid capital gains taxes on the sale.] By donating a business to support charitable causes, the entire amount of the sales proceeds goes to charity without diminishing any of it to pay income tax on the sale.

Here’s the key takeaway: if you sell a business or other asset and want to commit part or all of the proceeds to charitable causes, make the gift BEFORE you sell.

Marvin E. Blum

Marvin Blum in his “Liquidity Blazer,” reminding all who sell a business to consider making charitable gifts of a business interest BEFORE you sell the business.